- The Outdoors Crowd

- Posts

- The Rise Of YETI Coolers | Derek's Deep Dive

The Rise Of YETI Coolers | Derek's Deep Dive

The very first chapter of Derek's weekly Outdoors Industry insights, including industry trends, company deep dives and executive spotlight.

Derek O'Sullivan

April 16, 2024

Derek’s Deep Dive into The Outdoors: Chapter 1.

Welcome, and thanks for reading.

"What is the good of your stars and trees, your sunrise and the wind, if they do not enter into our daily lives?" – E.M. Forster

Key macro takeaways from Outdoors Industry Association participation trends

The outdoor recreation participant base grew 2.3% in 2022 to a record 168.1 million participants or 55 percent of the U.S. population ages six and older.

Although 2022 outdoor recreation included record numbers of participants and record-high participation rates, the number of outings per participant declined in 2022 for the first time since the pandemic began in 2020.

The new outdoor recreation participant base became more diverse in 2022 including increases in participation among Black, Hispanic, and LGBTQIA+ people.

Eighty percent of outdoor activity categories experienced participation growth in 2022, including large categories like camping and fishing and smaller categories like sport climbing and skateboarding.

My Take

It’s encouraging to see participation rates stay pretty much steady. I think everyone expected that they would drop violently post pandemic, although the drop in outings was reflected. As an industry, I feel we have a huge opportunity here. The pandemic reintroduced people to the outdoors. It’s up to us to keep them there in a sustainable fashion, with long term planning.

For me as a brand owner though, the question is: has everyone overspent on equipment during the last few years. And I think the answer is yes. There was a huge appetite and an influx of stock in 2021/22/23. Hence, at first principles, the need for product innovation has increased several-fold. And USP is even more key than ever.

Company Deep Dive - YETI Holdings, Inc.

Summary

Anyone that knows me, knows that I have been (mildly) obsessed with Yeti. It’s the phenomenal story of what is now a legendary brand. Its meteoric rise is one that will be hard to mimic. I love the story because there are crossovers with what we’re trying to do in CRUA. The Seiders addressed a problem of their own - they couldn't find a cooler that was tough enough for their ‘hook and bullet’ lifestyle, so they created one. They saw a commercial opportunity. And bingo. Well, not quite. There were ups and downs. In this chapter, we’re going to take a deep dive into Yeti. A little about the back story, but I want to dig deeper - from a business POV. What worked. What didn’t. What I learned when I visited them a couple of times, etc.

A little business backstory

It’s very hard to believe that the brand was only founded in 2006, by two Austin TX based brothers, with a little help from their father. The whole family were avid outdoorsmen and they speak a lot about spending a childhood in the wild. And that authenticity rings true today. When you visit their store in Austin (which has a lovely vibe - bar and all) you can’t miss the shallow water fishing boat in the middle of the floor. This is the industry that Roy Seiders used to design for.

In June 2015 Cortec, a mid-sized NY based PE firm bought a majority stake in Yeti, for an undisclosed sum. And in

Product strategy

‘Everything we make, we make it for ourselves first, and then we try to sell it.’

This really sums up the ethos that was there at the beginning. Yeti did one thing really well - better than anyone else. They designed the cooler box to solve a problem they knew existed. But that’s the easy part.

‘Ideas are like commodities…….unless you’re hanging around with someone who can bring them to life in front of you or take them to market.‘

And this is where there seemed to be a good balance between the brothers. The ideas man and the plan executor. Yeti kept plugging the same USP and secret sauce message for the first five years. Their video with a (rather tired looking) grizzly trying to open the cooler became a watershed moment for the brand. Link at the bottom. Am I being harsh on the bear??? I once met the PR team that ran this ‘experiment’, based in the Twin Cities, and the principal told me they came across the bear sanctuary almost by accident. But it was exactly on point. And the rest is history.

More recently, current CEO Matt Reintjes was quoted, “We have a high-quality customer and we are always looking for ways to create more opportunities to be a part of a consumer's life throughout the day.” In other words, they now have buy-in from an affluent market, so they’re finding ways to expand in complementary lines such as mugs, tumblers, buckets, chairs and much more. Thus increasing that vital LTV or lifetime value of their customers. Everyone in D2C knows how vital that statistic becomes.

Roy said many times that “I really felt like we educated our consumer on the selling points of our product. So when someone had a Yeti cooler in the back of their truck, they could defend that.” And that authenticity rang true in everything they did.

Partnerships and media content

“Almost overnight, YETI had created a small army of chatty brand ambassadors who spent their weekends engaging in conversations with other members of YETI’s target audience.”

This has been the core of the Yeti strategy from the start. Getting ‘buy in’ for the noisy outdoorsmen. And it has worked. Yeti avoided apathy from the start. They sought and got attention. The cost vs benefit conversation drove a lot of that early conversation, and it polarized the outdoors community for a while, which was perfect to drive conversations.

The Seiders’ were busy in the early days ensuring that possible customers could kick and feel the difference between their cooler and the competitions, thus showing it was not like for like. This is really difficult - practically creating their own segment through word of mouth. But again, there is a huge difference between Yeti and traditional coolers as pro wrestler ‘Big Bald Mike’ found out in the video below!

This strategy proved hugely instrumental in that early growth within the core community, thus building a strong and large base of true fans, online and offline.

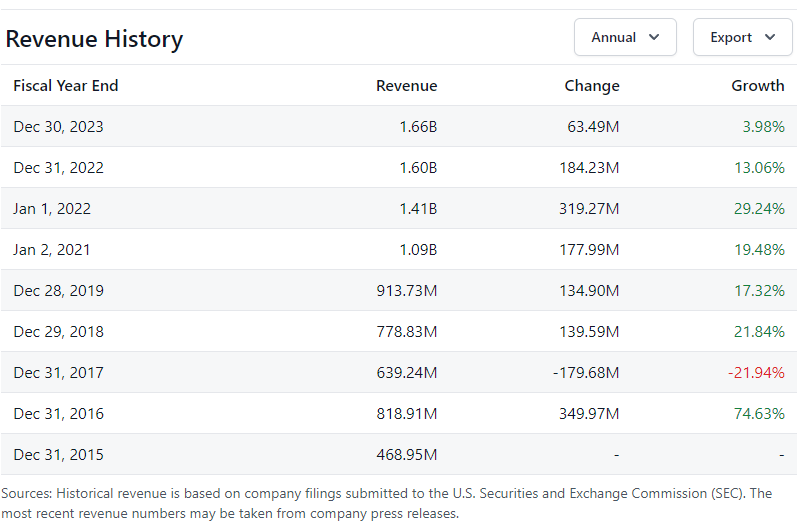

Revenue and ownership timeline

Yeti hit almost half a billion US$ in annual sales in under 10 years, which is almost a completely unheard of growth trajectory. While growth levels have kind of ‘normalized’ since then, that initial growth gave the brand amazing momentum.

By 2011, Yeti was selling more coolers than its suppliers could make. To meet the growing demand, they sold a majority stake in the company to the Cortec Group, a (relatively) small Manhattan based private equity firm, for a reported $67 million. This helped to accelerate the growth further, and reportedly added manufacturing capability. As we know, PE firms like to operate in 5 year cycles which probably propelled the movement towards IPO prep in 2016, which eventually materialized in 2019 after a false start.

At the time of writing Yeti is trading at $37.62 per share at a MKT Cap of $3.34Bn, after entering the market at $63 and reaching falsely inflated pandemic highs of $107. It holds a moderate buy consensus from analysts. I’m not a qualified financial advisor, and don’t have authority to speak to stock value, so do with that what you will.

Brick mortar vs online

In recent years, there has been a defined push on D2C with these results:

2015 - 8% online vs 2019 - 41% online vs 2022 q1 - 53% online

This aligned with total CAGR (compound annual growth rate) of 24% 2019 - 2022 means that things have been quite sound pre, during and post the pandemic, which is something that can’t be said for a lot of other outdoors brands, with most suffering huge dips in recent times. The company has said that D2C will continue to be a big part of their growth strategy moving forward.

Some bumps

Initial pricing. People told them they were absolutely nuts expecting a 10x price on existing coolers. And there was considerable resistance in the early years among partners to push the product.

NRA. NRA supporters’ problem with YETI started in 2018 …. when former NRA president Marion Hammer wrote a letter on behalf of the NRA-Institute for Legislative Action, saying that YETI had suddenly and without prior notice declined to do business with the NRA Foundation.

“They will only say they will no longer sell products to The NRA Foundation. That certainly isn’t sportsmanlike. In fact, YETI should be ashamed,” Hammer wrote. Next thing Yeti customers started, literally, blowing up their coolers, in a high profile social media hit job. The NRA eventually called a ceasefire when Yeti clarified that it was all a misunderstanding. I’d imagine there were a few sighs of relief in HQ.

Product recalls. Yeti has had its share of product recalls, most recently with the Yeti Coolers Hopper M30 Soft Cooler 1.0 and 2.0, Hopper M20 Soft Backpack Cooler and SideKick Dry Gear Case because of 1,400 reports of the magnet-lined closures failing, falling off or going missing which posed an ingestion risk. These sorts of thing are par for the course in successful companies, and this one seemed to be managed pretty well through a voluntary recall.

The future?

I’ve spoken with Matt Reintjes a couple of times and have been in email contact with him a bit. Without meeting him in person, he strikes me as a solid leader who certainly seems to inspire. I was at Yeti HQ once during an all hands and managed to eavesdrop a little. Without hearing the exact content, it was easy to see that he has a personable leadership style which suits the brand. For example, it’s not unusual to see flip flops and shorts around the office! But he was, overall, appointed for a reason. To drive shareholder value through growth. And that is happening, in a controlled fashion. I think the brand still has a lot of growing to do, and it’ll be interesting to see where it goes next. Geography is mapped, but I think its minor escapades into natural evolutions such as apparel have been very poor so far. when compared to others. And one has to feel that coolers and drinkware will reach a saturation point. So product strategy now becomes key. How do they increase that, without watering down the brand? Should lead to some interesting meetings between Jeff Beitz, head of brand, and Nathan Mack, head of product! Overall, steady as she goes is almost certainly the mantra…

In conclusion, why it worked and so many others didn’t

Starting with solving a real problem, that appealed to a large enough core audience.

Respect among the cornerstone audience.

This led to domain authority.

There was a realness and authenticity about what they did.

Strong gross margins in their pricing strategy.

Growth capital at key times

Allowed the potential customers to get hands on with the product, seeing the difference.

Addition of a strong D2C strategy once brand awareness had been achieved.

Smart and timely geographical extensions

Increase of LTV through increasing product range.

Amer Sports CEO Comments on Shift towards a more DTC Model

James Zheng provided several interesting details about the company, which owns Arc’teryx, Salomon, and other brands, and its strategy in a letter to shareholders as part of Amer’s annual report.

Parent company of Arc’teryx, Salomon, Atomic, Wilson, and other brands, filed its first annual report as a publicly traded company this week, after debuting on the NYSE on Feb 1st. The report 14 page is definitely worth scanning at least, and worth a greater time investment if you can. Read it here.

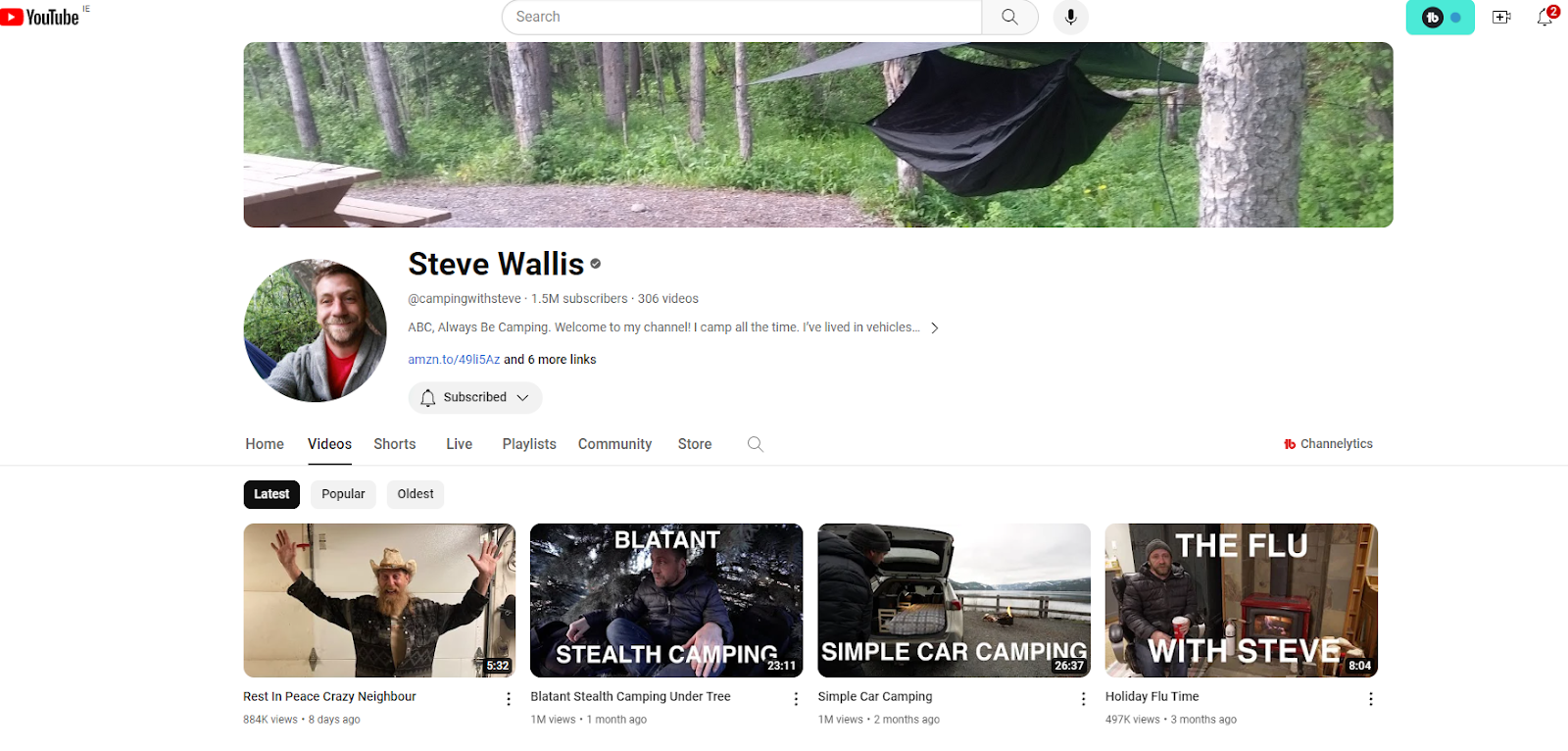

Trends - What’s trending on social media

Great to see Steve Wallis, AKA Steve Wallis, really nailing it on YouTube. He’s even trending on Google… Again, authenticity and real are the words that jump to mind with his content.

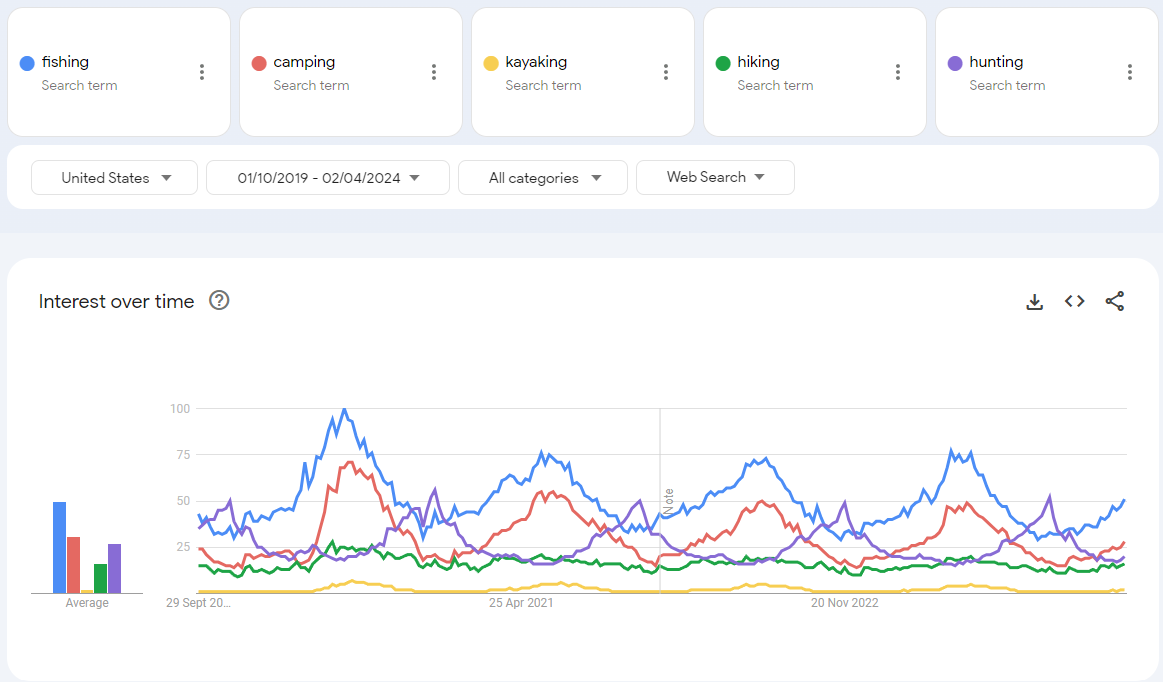

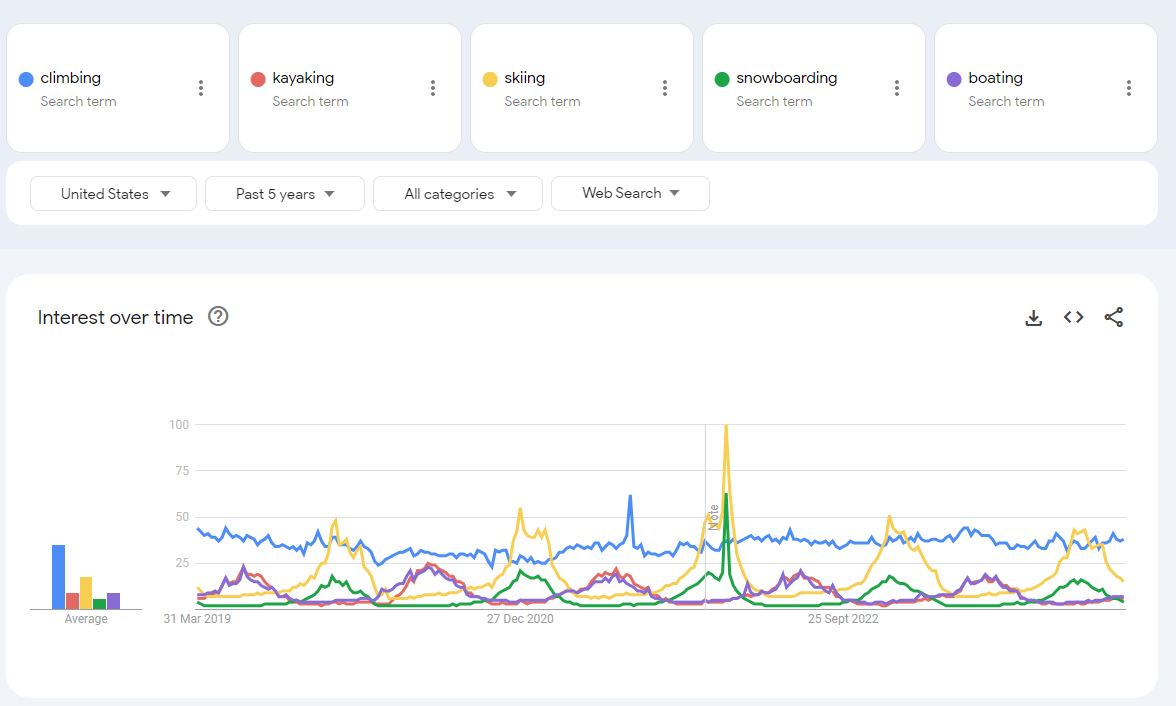

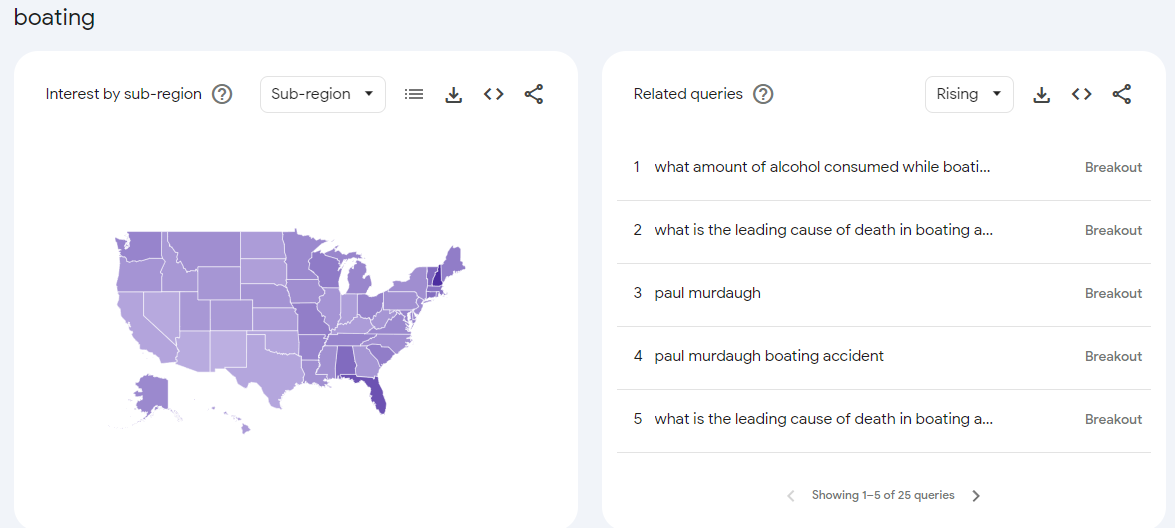

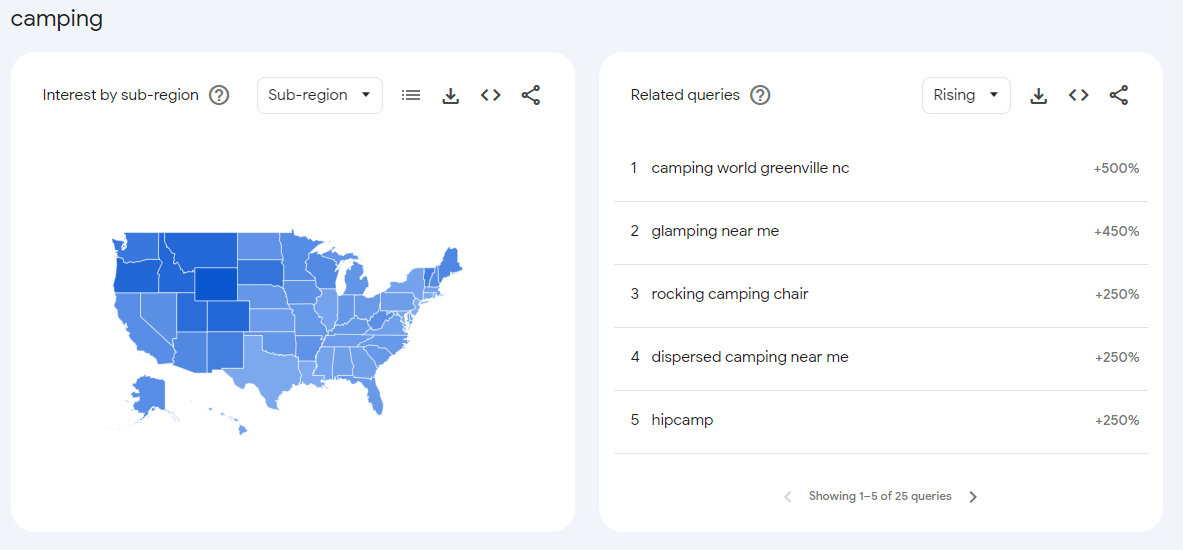

Search Trends

A few relevant insights from Google Trends.

Firstly, we can see the expected main category search volume is following expected seasonal search volume.

Here are some more, with kayaking providing the control between both, for reference, meaning it's just on both charts.

Notable opportunities from suggested breakouts:

I’ve noticed that there is a lot of interest in safe boating and safety in boating this quarter;

And, believe it or not, rocking camping chairs:

Derek’s & CRUA’s perspective

The business landscape has been challenging over the last 18 months or so. Over demand combined with under supply during Covid put a huge strain on supply chains. The big players over compensated in 2022/23 which led to market saturation and lots of discounted sales. Add to that the escalating raw materials costs and it’s in some ways, a perfect storm.

We examined possible diversification to Mexico, to be adjacent to the US. However the expertise just didn’t seem to be there, and where it was close, they still needed to source the material from China, so it somewhat defeated the purpose. Mexico’s supply chain is not as sophisticated as China’s. And this problem is replicated elsewhere. China’s prices are inflating as their production workforce ages, but they’re still the standard bearers.

But I do feel it just a matter of time before everyone, CRUA included, will have to look at ways of diversifying their supply chain, in order to tie up money for shorter periods. SHEIN has started examining this possibility for fashion. A kind of JIT manufacturing, but in D2C. Think of the huge upsides for whoever can pull it off?

Anyhow, that’s food for thought. I hope you enjoyed Chapter 1. Please share and spread the word. And please reply with any feedback or suggestions - always welcome. I want to make this newsletter the best it can be.

Derek.

Bibliography